Cardiothoracic Surgeon Compensation in a Low Volume Cardiac Surgery (LVCS) Setting: Part 1

Overview

Advances in coronary heart disease (CHD) prevention, diagnosis and treatment has...

For more than a decade, new heart program start-ups or expansions have been flat or declining in the US. This has occurred with a concomitant increase in the percentage of what has been termed “low volume heart programs” over the past 10-15 years. (see our previous blog Can Low Volume Cardiac Surgery Programs Be Excellent)

Recently, CFA has seen an increased interest by hospitals and health systems - operating in a wide variety of markets - to expand existing clinical service capabilities, capture new or out-migrated market share or to pursue first time entry into the cardiovascular services marketplace. Based on our strategic hospital heart services market profile/growth analysis, CFA predicted earlier this year the beginnings of an uptick in new and/or expanded cardiovascular program development in selected markets (see “Why Many Hospital CFO’s are More Optimistic About the Future”). With early growth already beginning, we believe a steeper growth curve will start to emerge in early 2018, this will mark the first “year over year” percentage increase in the expansion and/or development of new cardiac programs in many years.

This week’s topic of “The CFA Perspective” will examine the uptick in cardiac program expansion in the U.S. In this introductory post, we will explain why this trend is happening and how to identify the key indicators driving a potential start-up and/or expansion of cardiac programs. In Part 2, we will present a concise, detailed case study highlighting one of CFA client hospital’s cardiac services expansion initiative.

CFA’s business intelligence data and published reporting by other analysts show a minimum of 9-12 states with nearly 30 rural and 20 urban markets which are good candidates for new cardiovascular program starts ups and/or program expansion. For a large portion of hospitals in the U.S., cardiac services revenues, regardless of the reimbursement model, still represent the opportunity to generate significant contribution margins. Many CEOs, with little or no cardiovascular program capability, are becoming much more interested in keeping and/or re-directing more of their out-migrating cardiovascular business. Hence service expansion is often one of the means to getting there. CFA is currently assisting a number of hospitals and health systems with the evaluation and expansion of cardiac services capabilities and to reorganize their cardiac program operating model. The driving force behind each program expansion and re-structure project was “marketshare” and/or “growth“ driven.

One of our clients made the strategic decision to downsize their program 10 years ago. After seeing the substantial growth of their regional competitor facility in the cardiovascular arena over the past 5+ years, they engaged our firm to conduct a comprehensive cardiac market assessment and develop a plan ”to get back in the business of heart services.” Findings of the completed cardiac market assessment included documenting the substantial growth in the cardiovascular market, and that nearly 90% of the cardiac surgery and interventional cardiovascular business being performed by their competitor hospital was coming from the client’s primary and secondary service areas!

To assist hospitals assess whether they are candidates for developing or expanding their current cardiovascular capabilities footprint, CFA has developed a “Cardiovascular market assessment/profile” tool. This approach combines good old fashioned “boots on the ground” CFA senior staff interface with key hospital stakeholders, local and regional medical community, facilities and competitor landscape coupled with the use of a market assessment and financial analytic platform that analyzes all pertinent hospital data, provides insights into the hospital's regional cardiovascular disease incidence/prevalence rates, current and potential demand and volume migration and local/regional payer mix. This multi-factorial analysis leads to a set of key market indicators that assess the strength of hospital's “opportunity” or “candidacy” to engage in a successful cardiovascular services expansion initiative on a service-by-service basis. CFA is often retained to plan and assist with strategic plan formulation and implementation of new or expanding program development as well.

While the prevailing wisdom in the U.S. cardiovascular marketplace is the development of new heart programs are declining and volumes are contracting, CFA has a different perspective. While it is true the proliferation of heart programs in densely populated, urban environments has caused oversaturation, volume segmentation and dilution of those markets, there are an increasing number of small to medium-sized urban and rural marketplaces that are prime candidates to consider starting or expanding their cardiac services capability. In Part 2 of this series we will explore what makes a good candidate for cardiac services expansion and how CFA helped a health system decide to get back into the game!

As always, CFA invites your comments, suggestions and questions. For additional information, including strategies for developing new or expanded cardiac services, please call us at 1-949- 443-4005 or send us a confidential email at cfa@charlesfrancassociates.com.

Footnotes

Advances in coronary heart disease (CHD) prevention, diagnosis and treatment has...

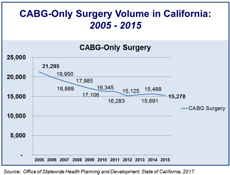

The national decline in cardiac surgical volumes is well documented: between 2000 and 2010, annual...